One more thing on money: the cost question only makes sense next to the return. A well-built payment or lending app in New York can move real transaction volume within the first year, and the compliance work that felt expensive up front is what lets you land enterprise partners and pass their security reviews. We’ve seen a clean SOC 2 posture unlock deals that a cheaper, non-compliant build simply couldn’t touch. Framed that way, security-first engineering isn’t a cost center — it’s what makes the product sellable. That return calculus is the real reason fintech app development in New York rewards doing it properly.

New York runs on money moving fast, and that pressure is exactly why fintech app development in New York rarely looks like building an app anywhere else. A payment hiccup in a small-town loyalty app is an annoyance. The same hiccup inside a Manhattan lending or trading product can trigger a regulator’s phone call. At KKRF Group, a top mobile app development company, we build financial products for startups and enterprises that have to survive that level of scrutiny. This guide is the honest version of what that takes — real costs, the features that actually matter, the build process, and the compliance work you can’t wave away.

We’ve watched teams burn six figures rebuilding apps that were never architected for New York’s rules. You don’t have to be one of them.

Key Takeaways

- Most fintech apps in New York cost between $30,000 and $400,000, driven mainly by compliance scope, integrations, and app type.

- Building compliance in from day one is far cheaper than retrofitting it — reactive fixes can cost 5x to 20x more.

- NYDFS, PCI-DSS, SOC 2, and KYC/AML aren’t optional extras in NYC; they shape your architecture.

- Cross-platform tools like Flutter and React Native cut cost and time-to-market, but high-security cores sometimes still call for native code.

- The right fintech app development company in New York is judged on its security track record and regulatory fluency, not its portfolio gloss.

What This Guide Covers

What Fintech App Development in New York Really Involves

Strip away the jargon and a fintech app is software that touches someone’s money. That’s the whole reason the stakes are higher. When your product holds a balance, initiates a transfer, or stores card data, you inherit a stack of obligations a photo-sharing app never has to think about.

The category is broad. In practice, most New York projects fall into a handful of buckets: a payment app or P2P payment app for moving cash between people, a digital wallet, a banking app or neobank, a lending app, a wealthtech app for investing, or a sprawling fintech super app that tries to do several at once. Each carries a different risk profile and a different price tag.

KKRF Group builds across all of these. Our engineering approach is security-first and enterprise-grade by default, because in financial software the architecture you choose on day one quietly decides how much you’ll spend on day 300.

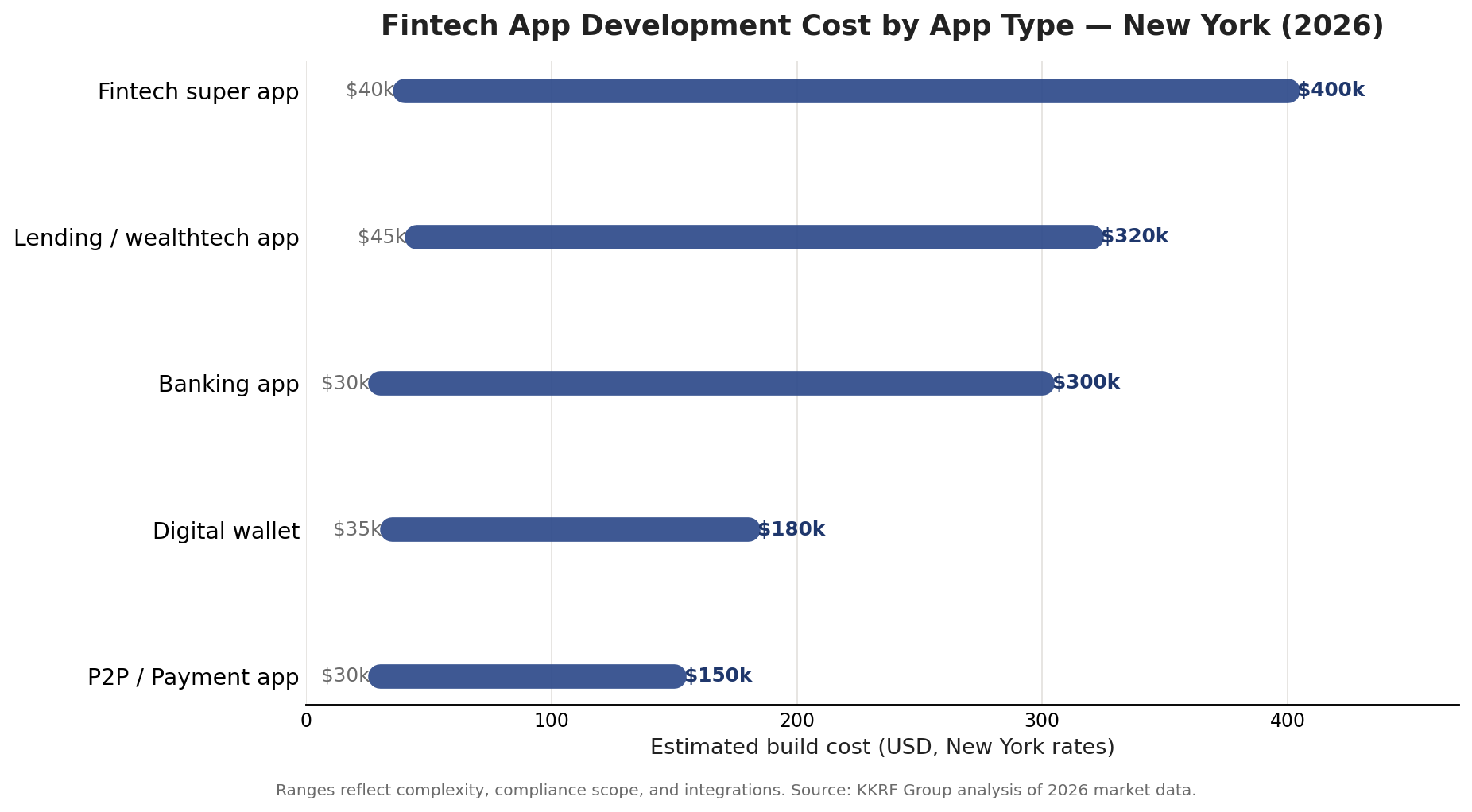

What It Costs to Build a Fintech App in New York

Here’s the number people actually want: a fintech app in New York usually lands somewhere between $30,000 and $400,000. That range is wide because a simple peer-to-peer payment tool and a full banking platform are barely the same species. New York rates run higher than most of the country — senior firms often bill $150 to $300 an hour, though plenty of shops sit in the $50 to $99 band.

Three things move the cost more than anything else: how much compliance work the product demands, how many third-party integrations it needs, and how complex the app type is. Proactive PCI-DSS work alone can add 15 to 25 percent to a build. That sounds steep until you price the alternative — bolting compliance on after launch runs 5 to 20 times more than doing it right the first time.

| App type | Typical NYC cost | Rough timeline | Biggest cost driver |

|---|---|---|---|

| P2P / payment app | $30k – $150k | 4 – 6 months | Payment gateway + fraud controls |

| Digital wallet | $35k – $180k | 5 – 7 months | Tokenization + multi-currency |

| Banking app / neobank | $30k – $300k | 6 – 10 months | Core banking + NYDFS compliance |

| Lending / wealthtech app | $45k – $320k | 7 – 11 months | Underwriting logic + SEC/FINRA rules |

| Fintech super app | $40k – $400k | 9 – 14 months | Multiple modules + integrations |

If you want a grounded figure for your own idea, the fastest path is a scoped estimate rather than a blanket quote — the cost to build a fintech app in NYC swings hugely on which of the rows above you actually live in. Scoping fintech app development in New York this way keeps the number honest.

The Features a New York Fintech App Actually Needs

Feature lists get bloated fast. We push clients toward the ones that earn trust and keep regulators satisfied, then layer the rest later. Every serious fintech app we ship includes most of the following.

- Secure onboarding with KYC/AML — identity verification and anti-money-laundering checks baked into signup, not tacked on.

- Biometric and multi-factor authentication — Face ID, fingerprint, and MFA as the default, not a settings-menu option.

- Tokenized payments — card data is tokenized through providers like Stripe, Adyen, or a PCI-compliant vault so you never store raw PANs.

- Real-time transactions and notifications — instant balance updates and push alerts, since a delayed money confirmation reads as a failure.

- End-to-end encryption and audit logs — data encrypted in transit and at rest, with a tamper-evident trail for every sensitive action.

- In-app support and dispute handling — because a payment problem the user can’t resolve is a churn event.

- Analytics dashboards — for the business side to watch fraud signals, retention, and transaction health.

Notice what’s not on that list: novelty. Fintech users don’t reward clever gimmicks. They reward an app that opens fast, shows the right balance, and never makes them wonder where their money went. Build the boring, trustworthy core first, then earn the right to add the flashy stuff.

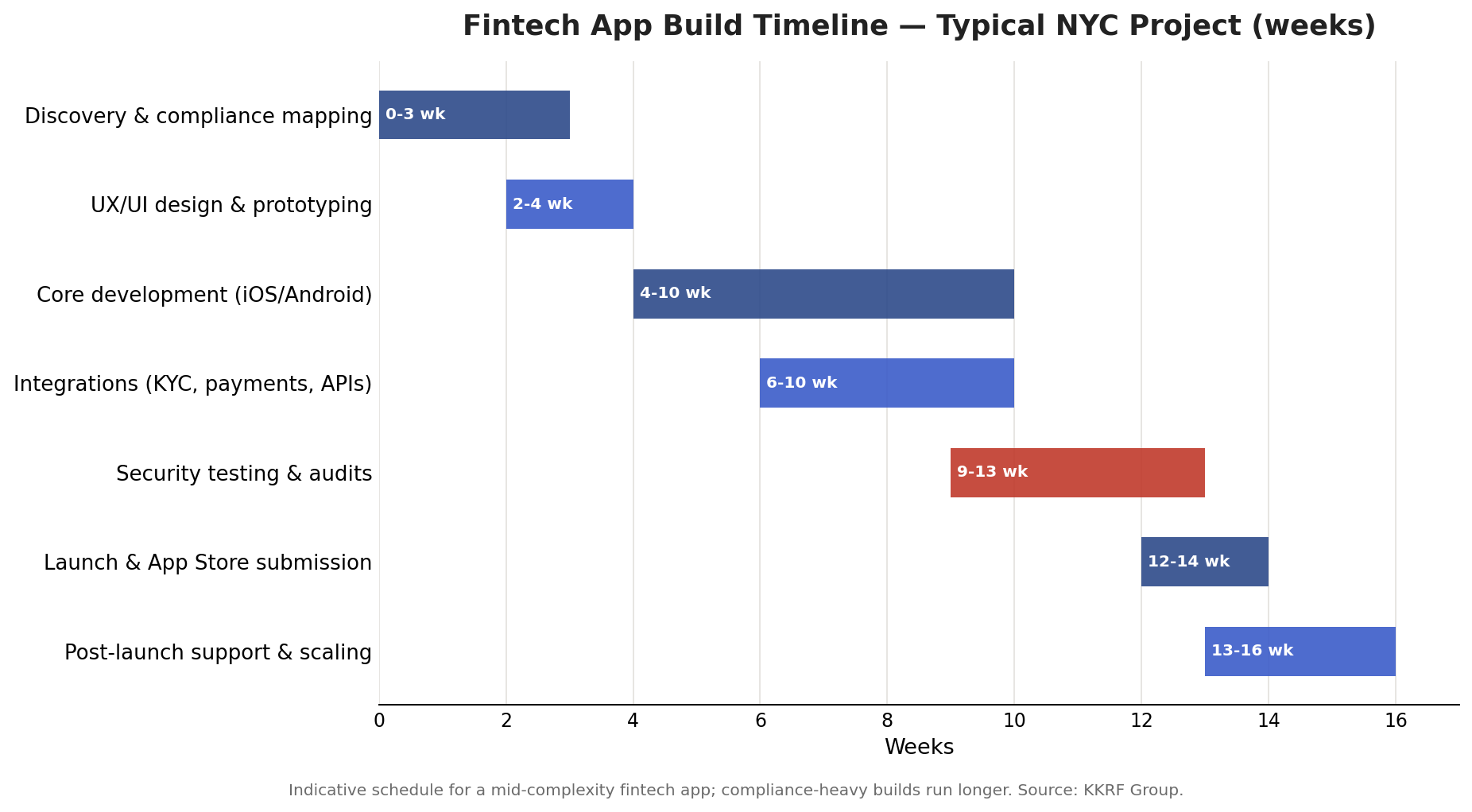

How We Build a Fintech App, Step by Step

Our approach to fintech app development in New York is deliberately front-loaded on compliance and architecture. That order isn’t bureaucratic — it’s what keeps the expensive surprises from showing up late.

- Discovery and compliance mapping. We identify which regimes apply — NYDFS, PCI-DSS, SEC/FINRA, SHIELD — before a single screen is designed. This is where most doomed projects go wrong by skipping ahead.

- UX/UI design and prototyping. Wireframes and clickable prototypes that make money movement feel calm and obvious. Financial anxiety is a design problem as much as a code one.

- Architecture and cloud-native setup. We design a scalable, cloud-native backend with the security boundaries drawn first, then the features poured in.

- Core development. iOS and Android builds proceed against the agreed architecture, using native or cross-platform code depending on the security and performance profile.

- Integrations. KYC providers, payment gateways, Plaid for bank connectivity, and any API integration the product depends on — each wired in and hardened.

- Security testing and audits. Penetration testing, code review, and a compliance audit against the frameworks mapped in step one.

- Launch and App Store submission. Financial apps face stricter store review, so we prepare documentation and privacy disclosures up front.

- Post-launch support and scaling. Monitoring, fraud tuning, and the infrastructure work to grow from hundreds of users to hundreds of thousands.

Have a fintech concept but no clarity on scope or compliance load? Our engineers will map the regulations and give you a realistic build plan. Start with our New York mobile app development team.

Request an Architecture Review →Compliance and Security: The Part You Can’t Skip in NYC

This is where New York earns its reputation. A fintech product operating here answers to more regulators than almost anywhere else in the country. Getting this wrong isn’t a slap on the wrist — penalties and remediation for a breach can run from six figures into the millions.

The frameworks you’ll most often need to design around:

- NYDFS (23 NYCRR 500) — New York’s cybersecurity regulation for financial services companies. If you operate here, this one usually applies.

- PCI-DSS — mandatory the moment you touch card data. Tokenization and no-PAN-storage designs keep your scope manageable.

- SOC 2 — the trust report enterprise partners and investors will ask to see before they integrate with you.

- SEC and FINRA — relevant for investing, brokerage, and wealthtech features.

- NY SHIELD Act — data-security obligations for any business holding New Yorkers’ private information.

- KYC / AML / BSA — identity and anti-money-laundering rules that shape onboarding and monitoring.

- HIPAA — only if your product blends finance with health data, but worth flagging early when it does.

Our security-first stance means these controls live in the architecture, not in a policy PDF nobody reads. For teams that need deeper coverage, we pair fintech builds with dedicated cybersecurity consulting. Standards bodies like the PCI Security Standards Council and the New York Department of Financial Services publish the requirements directly — worth reading before you scope.

Native vs Cross-Platform for Fintech Apps

One of the first real decisions is native versus cross-platform. There’s no universal winner — it depends on how security-sensitive your core is and how fast you need to ship. Here’s the honest comparison we walk clients through.

| Factor | Native (Swift / Kotlin) | Cross-platform (Flutter / React Native) |

|---|---|---|

| Performance | Best for heavy, real-time transaction loads | Excellent for most fintech use cases |

| Security control | Deepest access to platform security features | Strong, with some native modules for sensitive cores |

| Cost | Higher — two codebases | Lower — one shared codebase |

| Time-to-market | Slower | Faster |

| Best for | Trading, high-frequency, security-critical cores | MVPs, wallets, most consumer fintech apps |

In our experience, most New York startups are well served by Flutter or React Native, with a native module dropped in only where a security or performance edge case demands it. Enterprises with heavy trading workloads lean native more often.

Common Mistakes That Sink Fintech Apps

We get called in to rescue fintech apps often enough to see the same patterns. Avoid these and you’re already ahead.

- Treating compliance as a launch-week task instead of an architecture decision. This is the single most expensive mistake.

- Storing raw card or account data to “save time” — a decision that balloons PCI scope and breach liability.

- Choosing the cheapest team over the one with a real security track record. In fintech, cheap builds get rebuilt.

- Skipping penetration testing before launch and finding out about the holes from an attacker instead.

- Building a super app before proving a single core loop. Scope discipline beats feature sprawl every time.

How to Choose a Fintech App Development Company in New York

When you evaluate a fintech app development company in New York, portfolio screenshots tell you almost nothing. What matters is whether they can talk fluently about the things that break financial products. Anyone serious about fintech app development in New York should pass this quick framework.

| Ask this | What a strong answer sounds like |

|---|---|

| How do you handle PCI scope? | Tokenization, no PAN storage, clear vault strategy |

| Which NY regulations have you built against? | Names NYDFS, SHIELD, SEC/FINRA without hesitation |

| Native or cross-platform, and why? | A reasoned answer tied to your app, not a default |

| What does post-launch support include? | Monitoring, fraud tuning, scaling — not just bug fixes |

| Can we see your security process? | Pen testing and audits described as standard, not upsell |

This is also where the in-house versus outsourced question comes up. Hiring fintech developers in New York directly gives you control but is slow and expensive to staff; an experienced partner gets you a full team and compliance experience immediately. KKRF Group works as a long-term technology partner rather than a code vendor — which, for a regulated product, tends to matter more than the day-one hourly rate. Our broader mobile app development services cover the full lifecycle, and complex financial platforms often lean on our SaaS development work too.

Where NYC Fintech Is Heading

New York’s fintech scene doesn’t sit still, and a few shifts are worth building toward rather than around. Embedded finance is pushing payment and lending features into non-financial apps. AI-driven fraud detection is moving from nice-to-have to table stakes. Open banking, powered by aggregators like Plaid, keeps lowering the friction of connecting accounts.

Further out, blockchain rails and stablecoin settlement are creeping into serious conversations on Wall Street, and AI-driven agentic finance — software that acts on a user’s behalf within set limits — is the frontier a lot of Brooklyn and Manhattan startups are prototyping right now. None of it changes the fundamentals: build secure, stay compliant, earn trust.

Ready to put real numbers and a timeline against your fintech idea? Talk to the engineers who build these products for New York’s toughest requirements. Tell us what you’re building.

Get a Custom Project Estimate →Frequently Asked Questions

How much does it cost to build a fintech app in New York?

Most fintech apps in New York cost between $30,000 and $400,000. A simple P2P payment app sits at the lower end, while a full banking platform or fintech super app reaches the top. Compliance scope, integrations, and app complexity are the biggest cost drivers.

How long does it take to build a fintech app?

A straightforward fintech app typically takes 4 to 6 months. More complex banking, lending, or super apps run 7 to 14 months once compliance mapping, integrations, and security audits are factored in.

What compliance is required for fintech apps in New York?

It depends on the product, but common requirements include NYDFS (23 NYCRR 500), PCI-DSS for card data, SOC 2, KYC/AML rules, the NY SHIELD Act, and SEC/FINRA rules for investing features. Mapping these before development starts is essential.

Should I build a native or cross-platform fintech app?

Most consumer fintech apps do well on Flutter or React Native, which cut cost and time-to-market. Trading platforms or security-critical cores sometimes justify native Swift or Kotlin, or a hybrid with native modules for the sensitive parts.

Is it better to hire fintech developers in New York or outsource?

Hiring in-house gives you direct control but is slow and costly to staff with compliance-experienced engineers. Partnering with an experienced fintech app development company gets you a full team and regulatory experience immediately, which usually wins for regulated products.

What features does a fintech app need?

At minimum: secure KYC/AML onboarding, biometric and multi-factor authentication, tokenized payments, real-time transactions and notifications, end-to-end encryption with audit logs, and in-app support. Analytics and dispute handling follow closely behind.

Fintech is unforgiving of shortcuts, and New York is the least forgiving market of all. Build it right the first time with a partner who lives in this world. See how we build for New York.

Book a Discovery Call →