Launching a financial product in the five boroughs means building for the most demanding users, regulators, and investors in the world. FinTech app development in New York sits at the intersection of hard engineering and hard regulation, and getting either wrong is expensive. As a top mobile app development company, KKRF Group builds fintech products where security and compliance are designed in from day one, not bolted on before launch.

This guide breaks down what it actually costs, how long it takes, which regulations apply in New York specifically, the tech stack that holds up under audit, and how to pick a fintech app development company in New York that will still be a good decision two years after launch.

Quick Answer: FinTech App Development in New York

Quick Answer: Building a FinTech app in New York generally costs between $70,000 for a compliant MVP and $250,000 for a market-ready product, with advanced platforms exceeding $450,000. Timelines run 6 to 18 months. The cost is driven less by screens and features than by regulatory scope, because New York fintech apps must satisfy NYDFS Part 500, the NY SHIELD Act, PCI DSS v4.0.1, and usually SOC 2 Type II. The right development partner is one that treats KYC/AML, encryption, and auditability as architecture, not paperwork.

Key Takeaways

- A FinTech app built to New York standards typically costs $70,000 for an MVP and $120,000–$250,000 for a market-ready product, with advanced platforms running $250,000–$450,000+.

- Compliance is not a line item you add later. Security and regulatory work absorbs 25–40% of a fintech budget, and in New York that means NYDFS Part 500, the NY SHIELD Act, PCI DSS v4.0.1, and SOC 2.

- Most New York fintech apps take 6 to 18 months from discovery to launch, depending on how much regulated functionality ships in version one.

- NYC engineering rates run $120–$250 per hour at the agency level, which is why architecture decisions made early have an outsized effect on total cost.

- Choosing a partner in New York gives you proximity to regulators, banking-integration talent, and investors, but the real selection criteria are security track record and compliance fluency, not location alone.

What This Guide Covers

- Quick Answer

- Why New York Is a Different Build

- FinTech App Types & Complexity

- What It Costs in New York

- Where the Budget Goes

- NY Compliance: NYDFS, PCI, SOC 2

- The FinTech Tech Stack

- The Development Process

- Security-First Architecture

- Common Mistakes to Avoid

- How to Choose a Partner

- Future Trends

- FAQs

FinTech app development is the design, engineering, and compliance work required to build a mobile or web application that moves, stores, or manages money and financial data. Unlike a typical consumer app, a fintech product carries legal duties around data protection, identity verification, and transaction integrity from its very first release. That single difference reshapes the budget, the timeline, and the team you need.

Why New York Is a Different Kind of FinTech Build

New York is the financial capital of the United States, and that changes the engineering brief before a single screen is designed. A payment or banking app used in Manhattan or Brooklyn is likely to touch regulated money movement, which pulls it under both federal rules and New York’s own financial regulator. We’ve seen founders underestimate this and discover mid-build that their “simple” wallet app needed a compliance architecture closer to a bank’s.

Proximity matters here in practical ways. New York gives fintech teams direct access to banking partners, payment networks, compliance counsel, and the venture investors who fund financial products. When a build question turns into a regulatory question, being in the same time zone as your bank sponsor and your NYDFS-savvy lawyer shortens the loop. That is a real reason companies search for fintech app development services in New York rather than defaulting to the cheapest offshore quote.

The trade-off is cost. New York fintech app developers command premium rates because the talent pool understands banking integrations, KYC/AML flows, and audit expectations that a general app shop does not. Senior mobile engineers in NYC bill $150 to $250 per hour, and full-service agencies quote $120 to $250 per hour. Those numbers are defensible when the work involves regulated money, and dangerous when a vendor charges them without the compliance experience to match.

What Counts as a FinTech App? Categories and Complexity

“FinTech app” covers a wide range of products, and where yours lands on that range is the single biggest predictor of cost. A budgeting tool and a full neobank are both fintech, but they are not remotely the same build. Sorting your idea into the right category early prevents the most common budgeting mistake: pricing a complex, regulated product as if it were a simple content app.

Neobank / digital banking app: A neobank is a mobile-first banking product that offers accounts, cards, and payments without a physical branch, usually on top of a sponsor bank’s charter. It is among the most complex and regulated fintech categories because it handles deposits, card issuance, and real-time money movement.

Payment app: A payment app lets users send, receive, or accept money, often connecting to card networks and bank rails. Because it processes cardholder data, it falls squarely under PCI DSS and demands tokenization and strong transaction security from day one.

Lending app: A lending app originates or services loans, running credit checks, underwriting, and repayment schedules. Its complexity comes from decisioning logic, fair-lending obligations, and integrations with credit bureaus and bank accounts.

WealthTech and robo-advisor: WealthTech apps manage investments, and a robo-advisor automates portfolio decisions using rules or models. These products carry securities-related obligations and need reliable market-data integrations and airtight calculation logic.

InsurTech app: An InsurTech app digitizes quoting, underwriting, policy management, or claims for insurance products. It blends heavy workflow logic with sensitive personal data, so privacy controls and document handling dominate the build.

| App type | Typical complexity | New York cost range (2026) | Indicative timeline |

|---|---|---|---|

| Personal finance / budgeting | Low–Medium | $70k–$130k | 5–8 months |

| Payment / wallet app | Medium–High | $120k–$250k | 7–12 months |

| Lending / BNPL platform | High | $180k–$350k | 9–15 months |

| Neobank / digital banking | Very High | $250k–$450k+ | 12–18 months |

| WealthTech / robo-advisor | High | $200k–$400k | 10–16 months |

| InsurTech platform | Medium–High | $150k–$320k | 9–15 months |

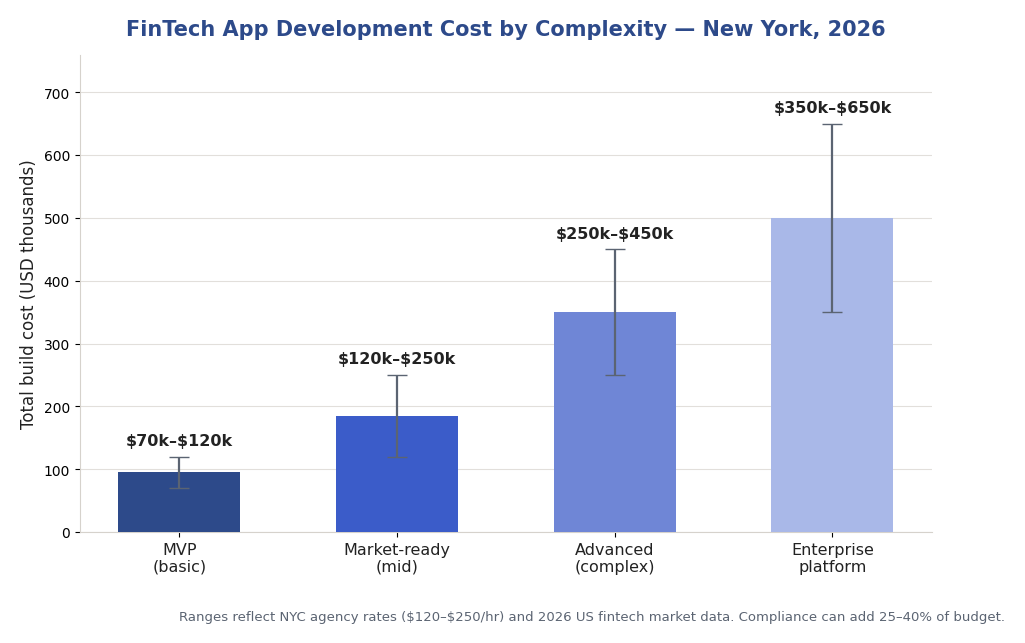

How Much Does It Cost to Build a FinTech App in New York?

The cost to build a fintech app in New York generally ranges from $70,000 for a compliant MVP to $450,000 or more for an advanced, fully regulated platform. A market-ready product with real users and audited controls usually lands between $120,000 and $250,000. These figures reflect 2026 New York agency rates and the reality that fintech carries a heavier compliance load than most app categories.

Three variables move the number most: how much regulated money movement the app handles, how many third-party integrations it needs, and how deep the compliance requirements run. A budgeting app that only reads data is cheap. A wallet that moves funds, verifies identity, and stores card data is not, because each of those capabilities adds engineering and audit work.

New York rates are a multiplier on all of the above. At $120 to $250 per hour, an extra month of scope is $20,000 to $40,000, so decisions about what ships in version one have direct budget consequences. This is why disciplined scoping, not cutting corners on security, is the honest way to control fintech cost.

| Build tier | What you get | New York cost (2026) | Timeline |

|---|---|---|---|

| MVP | Core flow, one platform, essential KYC and security | $70k–$120k | 6–9 months |

| Market-ready | Multi-feature, iOS + Android, audited controls | $120k–$250k | 9–14 months |

| Advanced platform | Deep integrations, multiple user roles, full compliance | $250k–$450k+ | 12–18 months |

The chart below shows how New York fintech build costs scale with complexity, using 2026 market ranges. Treat the bars as planning anchors, not quotes; a precise number always comes out of a scoping exercise against your specific feature list and compliance scope.

Figure 1: FinTech app development cost by complexity in New York, 2026.

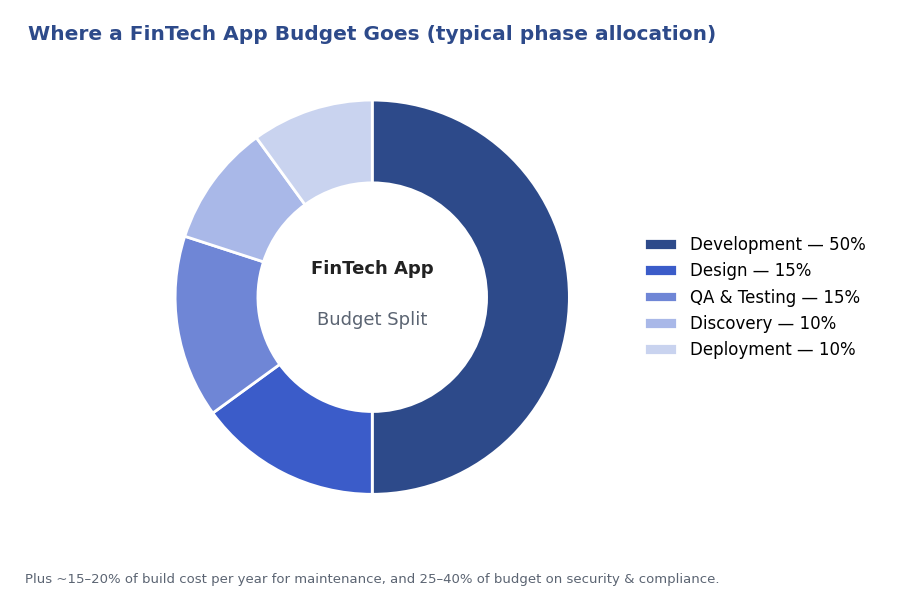

Where the Budget Goes: Cost Breakdown and Hidden Costs

Understanding where a fintech budget actually goes helps you spot a padded quote and a naive one. Across a typical build, development consumes about 50% of the budget, design 15%, QA and testing 15%, discovery 10%, and deployment 10%. Fintech shifts weight toward QA and security because a bug in money movement is not a cosmetic problem.

Compliance is the cost most first-time founders miss. Security and regulatory work often absorbs 25% to 40% of a fintech budget, and some of it is external. A SOC 2 Type II audit runs roughly $30,000 to $80,000, and a PCI DSS Level 1 assessment by a Qualified Security Assessor can cost $50,000 to $150,000 before any remediation. Budgeting these late is how projects blow through their reserves.

Then there is the cost after launch. Plan on 15% to 20% of the original build cost per year for maintenance, security patching, and dependency updates. Ongoing compliance monitoring tooling adds another $15,000 to $40,000 annually. A fintech app is a living system under constant regulatory and threat pressure, and the budget has to reflect that.

Figure 2: Typical phase allocation of a FinTech app budget.

Not sure whether your idea is a $90k MVP or a $300k platform? A short scoping conversation usually settles it. Our team can map your feature list to a realistic New York budget and compliance scope. See how we build mobile apps in New York.

Get a Custom Project Estimate →FinTech Compliance in New York: NYDFS, PCI DSS, SOC 2, KYC/AML

Compliance is where New York fintech projects succeed or quietly fail. New York regulates financial technology more aggressively than most states, and a product that moves money for New York users inherits obligations that a general app never faces. As a security-first engineering company, KKRF Group treats each of these frameworks as an architecture requirement rather than a checklist to satisfy near launch.

NYDFS Part 500 (23 NYCRR 500): This is the New York Department of Financial Services cybersecurity regulation that applies to financial institutions and their technology partners operating in the state. It mandates a written security program, encryption of nonpublic information, multi-factor authentication, incident reporting, and a designated security officer. If your app serves a New York financial entity, its requirements shape your architecture.

NY SHIELD Act: The Stop Hacks and Improve Electronic Data Security Act requires any business holding the private data of New York residents to maintain reasonable administrative, technical, and physical safeguards. It applies broadly, not just to licensed financial firms, so most consumer fintech apps with New York users fall under it.

PCI DSS v4.0.1: The Payment Card Industry Data Security Standard governs any app that stores, processes, or transmits cardholder data. Version 4.0.1 is now fully mandatory after the v3.2.1 transition ended in March 2025, and it pushes teams toward continuous validation rather than once-a-year checks. The practical implication is tokenization and keeping raw card data off your own servers wherever possible.

SOC 2 Type II: A SOC 2 Type II audit independently verifies that your security controls operate effectively over a 6-to-12-month period across trust criteria like security, availability, and confidentiality. Enterprise customers and banking partners frequently require it before they will integrate, which makes it a commercial gate, not just a compliance one.

KYC and AML: Know Your Customer and Anti-Money-Laundering rules require verifying user identity and monitoring transactions for suspicious activity. In practice this means integrating identity-verification and screening services and building the audit trails regulators expect. These flows are core product features in most fintech apps, not optional add-ons.

| Framework | What it covers | Who it hits | Rough external cost |

|---|---|---|---|

| NYDFS Part 500 | Cybersecurity program for NY financial entities | Apps serving NY financial firms | Internal program + audits |

| NY SHIELD Act | Reasonable safeguards for private data of NY residents | Most apps with NY users | Built into architecture |

| PCI DSS v4.0.1 | Cardholder data security | Any app touching card data | QSA assessment $50k–$150k |

| SOC 2 Type II | Operating effectiveness of controls | Apps selling to enterprises/banks | Audit $30k–$80k |

| KYC / AML | Identity and transaction monitoring | Money-movement apps | Per-verification vendor fees |

The FinTech Tech Stack: Mobile, Backend, Cloud, and Integrations

The right stack for a fintech app balances speed of delivery against the reliability and auditability that regulated money demands. There is no single correct answer, but there are well-worn, defensible choices. Below is the stack we reach for on most New York fintech builds, and why.

On mobile, the choice usually comes down to React Native or Flutter for cross-platform builds, or native Swift and Kotlin when performance and platform-specific security features justify the cost. React Native lets a team share code across iOS and Android while dropping to native modules for sensitive operations, which is often the pragmatic middle ground for a fintech MVP.

| Consideration | React Native | Flutter | Native (Swift/Kotlin) |

|---|---|---|---|

| Code sharing | iOS + Android from one codebase | iOS + Android from one codebase | Separate per platform |

| Best for | MVPs, faster time-to-market | Custom UI, smooth animations | Max performance and security depth |

| Talent pool in NYC | Very large | Growing | Large but pricier |

| Fintech fit | Strong with native modules | Strong, newer ecosystem | Strongest for high-security apps |

On the backend, Node.js, Python with Django, Java with Spring Boot, and Go all appear in production fintech systems; the pick depends on team strength and throughput needs. PostgreSQL is the default for transactional financial data because of its integrity guarantees, with Redis for caching and sometimes MongoDB for flexible, non-transactional data. For payments and banking connectivity, teams lean on Stripe, Plaid, and Adyen rather than building card and bank integrations from scratch.

The cloud layer is where compliance and engineering meet. AWS Financial Services, Microsoft Azure, and Google Cloud all offer PCI-aligned infrastructure, immutable audit logs, and secrets management. Pairing that with biometric authentication, end-to-end encryption, and tokenization gives you the security posture a New York fintech audit expects. The stack should be boring in the best way: proven components, wired together with discipline.

The FinTech App Development Process: Discovery to Launch

A disciplined process is what keeps a regulated build on budget. The sequence below is how experienced New York fintech teams move from idea to a live, audited product. Each step exists to remove risk before it becomes expensive.

Step 1 — Discovery and compliance scoping. Before design, the team maps features to regulatory obligations and defines which frameworks apply. This is where NYDFS, PCI, and KYC/AML scope get set, and where a realistic budget and timeline first take shape.

Step 2 — UX and product design. Designers turn the scoped requirements into flows and interfaces, paying special attention to onboarding, identity verification, and transaction screens. Good fintech design reduces support cost and drop-off, so it earns its 15% of budget.

Step 3 — Architecture and security design. Engineers define the data model, encryption strategy, tokenization approach, and cloud topology. Decisions made here determine whether the app can pass an audit later, which is why security is designed before feature code is written.

Step 4 — Development. The team builds the app in iterative sprints, wiring in payment, banking, and identity integrations behind secure APIs. Money-movement code gets the most review because its failure modes are the most costly.

Step 5 — QA, security testing, and compliance validation. Beyond functional testing, the app goes through security testing, penetration testing, and control validation against the target frameworks. This stage is heavier for fintech than for a typical app, and skipping it is how breaches happen.

Step 6 — Deployment and launch. The app ships to the App Store and Google Play with monitoring, logging, and incident response in place. Launch is the start of the compliance lifecycle, not the end of the project.

Step 7 — Maintenance and continuous compliance. After launch, the team patches dependencies, monitors threats, and maintains audit readiness as regulations evolve. Budgeting 15% to 20% of build cost per year keeps the product secure and current.

Security-First Architecture: How KKRF Group Builds FinTech Apps

KKRF Group approaches fintech as a security problem that happens to have a user interface. Every build starts with a threat model and a compliance map, so that encryption, access control, and auditability are architectural decisions rather than late additions. This is the difference between an app that passes its first audit and one that has to be partially rebuilt to pass it.

Our engineering approach favors proven, enterprise-grade components over novelty: PostgreSQL for transactional integrity, tokenization to keep card data out of scope, and cloud-native infrastructure with immutable logging. We build KYC, AML, and consent flows as first-class product features, and we design APIs so that sensitive operations are isolated, monitored, and reversible where they should be.

Because we work as a long-term technology partner, we optimize for what the product costs to run and audit over years, not just what it costs to ship. That means transparent development, documentation an auditor can follow, and an architecture that a New York fintech company can grow into rather than out of. For teams weighing a broader engineering relationship, our mobile app development services extend well beyond the initial launch.

Common Mistakes in FinTech App Development

Most fintech budget overruns trace back to a small set of avoidable mistakes. We have watched each of these turn a healthy project into a stressed one. Naming them early is the cheapest insurance you can buy.

- Treating compliance as a launch-week task. Retrofitting NYDFS, PCI, or SOC 2 controls costs several times more than designing for them, and it can delay launch by months.

- Underscoping the MVP. Trying to ship a neobank feature set on an MVP budget produces an app that is neither cheap nor finished.

- Storing card or bank data you do not need. Holding sensitive data expands your PCI scope and your breach risk; tokenization and third-party vaults exist for a reason.

- Choosing a vendor on price alone. A general app shop at a low rate often lacks the compliance experience, and the rework erases the savings.

- Ignoring post-launch cost. A fintech app without a maintenance and monitoring budget degrades into a security liability within a year.

- Skimping on QA and penetration testing. In fintech, an untested edge case in money movement is not a bug report, it is an incident.

Compliance questions are cheaper to answer before you write code than after an audit flags them. Bring us your product idea and we will pressure-test its NYDFS, PCI, and SOC 2 implications. Explore our cybersecurity and compliance work.

Request an Architecture Review →How to Choose a FinTech App Development Company in New York

Choosing a fintech development partner is a risk decision more than a shopping decision. The wrong pick shows up not as a bad demo but as a failed audit or a breach a year later. Use the framework below to separate a genuine fintech partner from a general app shop with a fintech landing page.

When to choose a New York fintech development partner: Pick a New York firm when your product moves regulated money, serves New York financial entities, or needs close coordination with local banking partners, investors, and compliance counsel. The premium rate is justified when the work genuinely requires NYDFS, PCI, and KYC/AML fluency.

When a New York partner may not be necessary: If your product is a low-risk informational or budgeting tool that never touches card or bank data, you may not need a premium New York fintech specialist. In that case, general mobile app development talent can deliver at a lower cost without meaningful added risk.

What to evaluate: Look for a demonstrable security and compliance track record, a documented development and testing process, transparent pricing tied to scope, relevant integration experience with payment and banking providers, and a concrete post-launch maintenance plan. Ask how they would handle your specific compliance scope; a real partner answers in specifics, not slogans.

Known limitations to accept: No partner can promise a fixed price on a moving regulatory target, and any firm that guarantees a flat fintech quote before scoping is either padding heavily or planning to cut corners. Expect a scoping phase, expect compliance to shape the budget, and treat those as signs of honesty rather than red flags.

Recommendation: Shortlist partners on security and compliance evidence first, price second. For a regulated New York fintech product, an experienced, security-first partner like KKRF Group that designs for audit from day one will almost always cost less over the product lifecycle than a cheaper vendor whose work has to be remediated.

Future Trends in FinTech App Development

FinTech in 2026 is being reshaped by a few durable forces, and the products that account for them now will age better. AI is moving from a feature to an expectation, embedded finance is spreading into non-financial apps, and regulators are tightening the bar on data security. Building with these trends in mind protects your investment.

AI and machine learning are becoming standard for fraud detection, credit scoring, and personalized financial guidance, while regulators watch model transparency closely. Embedded finance and open-banking connectivity through providers like Plaid are letting any app offer payments or accounts, which expands both opportunity and compliance scope. Meanwhile, the shift to continuous PCI validation and stricter state privacy laws means security is trending toward always-on rather than annual.

Building the Right Way in New York

FinTech app development in New York is expensive for a reason: the products carry real regulatory and security weight, and the city holds the talent that knows how to carry it. Get the scoping and compliance decisions right early, budget honestly for security and maintenance, and choose a partner on track record rather than price. Do that, and a New York fintech build becomes a durable asset instead of a liability waiting for its first audit.

If you are ready to move from budgeting to building, let us scope your New York fintech app end to end, from compliance map to launch plan. Work with our New York mobile app team and get a plan you can actually fund.

Talk to Our Engineering Team →Frequently Asked Questions

How much does it cost to build a fintech app in New York?

A fintech app built to New York standards typically costs $70,000 to $120,000 for a compliant MVP, $120,000 to $250,000 for a market-ready product, and $250,000 to $450,000 or more for an advanced platform. Compliance work alone can account for 25% to 40% of the total budget.

How long does it take to develop a fintech app?

Most New York fintech apps take 6 to 18 months from discovery to launch. A focused MVP with core KYC and security can ship in 6 to 9 months, while a neobank or heavily regulated platform runs 12 to 18 months.

What compliance do fintech apps in New York need?

A New York fintech app generally must address NYDFS Part 500 (23 NYCRR 500), the NY SHIELD Act, PCI DSS v4.0.1 if it touches card data, and SOC 2 Type II for enterprise integrations. KYC and AML identity and transaction-monitoring flows are usually built directly into the product.

Which tech stack is best for a fintech app?

A common, defensible fintech stack pairs React Native or Flutter on mobile with a Node.js, Python, Java, or Go backend, PostgreSQL for transactional data, and PCI-aligned cloud infrastructure such as AWS Financial Services. Payment and banking connectivity is handled through Stripe, Plaid, or Adyen rather than built from scratch.

How do I choose a fintech app development company in New York?

Prioritize a proven security and compliance track record over price. Ask for evidence of PCI, SOC 2, and KYC/AML experience, a clear development and testing process, transparent pricing, and a plan for post-launch maintenance. Location in New York helps with regulator and banking proximity, but compliance fluency is the real selection criterion.

Should I start with an MVP or a full fintech platform?

Most teams should start with a compliant MVP that ships one core money-movement flow with essential security and KYC, then expand. This controls cost, validates demand, and still satisfies the non-negotiable regulatory baseline that fintech requires from day one.