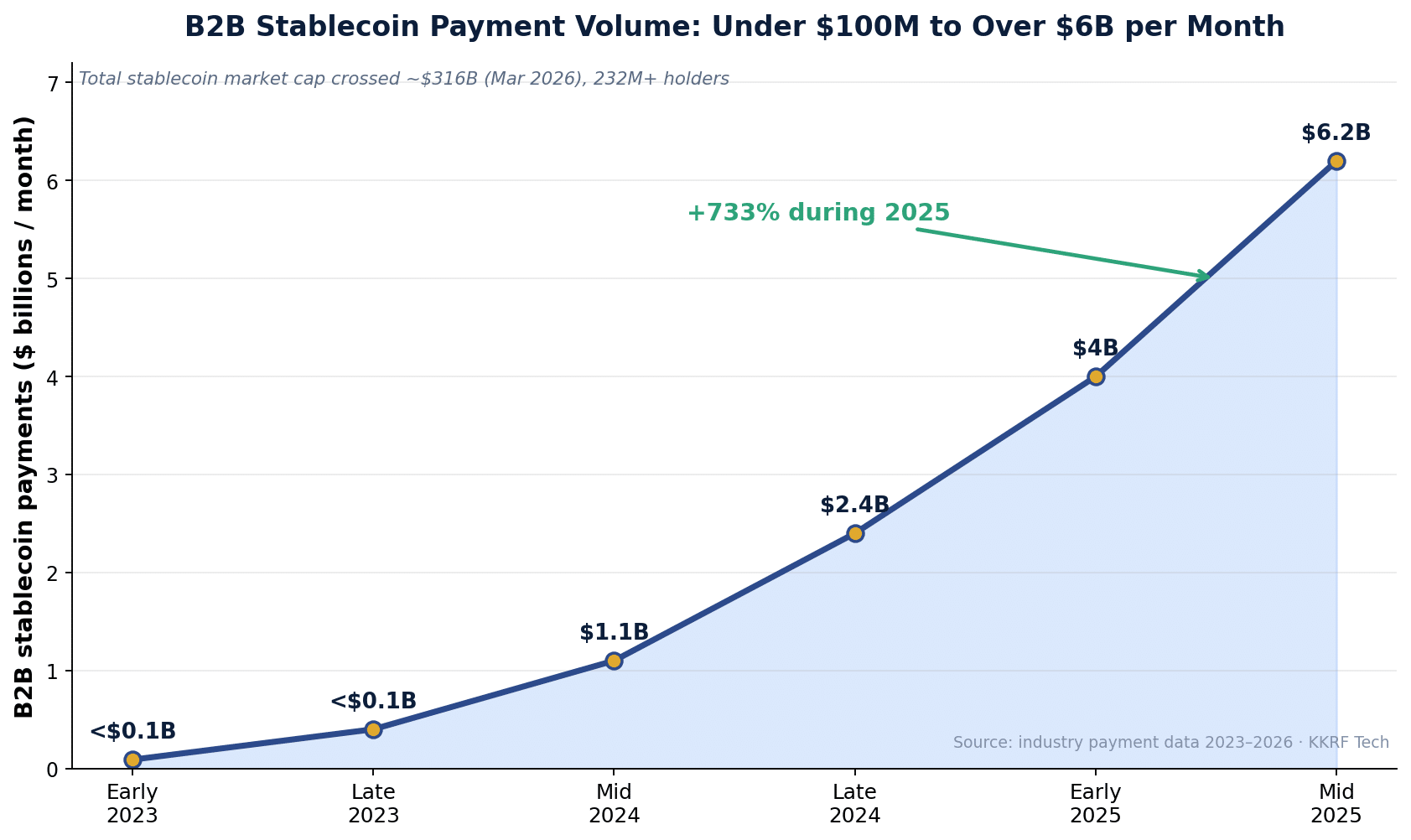

Stablecoin payment integration has moved from crypto experiment to enterprise treasury strategy in under three years. B2B stablecoin payments surged more than 700% during 2025, climbing from under $100 million a month in early 2023 to over $6 billion a month by mid-2025. Finance and engineering teams are no longer asking whether digital-dollar rails work — they are asking how to wire them into existing ERP, treasury, and accounts-payable systems without breaking compliance.

This resource explains how stablecoin payment integration actually works at enterprise scale: the reference architecture, what it costs versus card and wire rails, the GENIUS Act and MiCA obligations that now govern it, and how to decide whether it belongs in your payment stack. Every figure here is drawn from current 2026 market data and primary regulatory sources, with the trade-offs stated plainly.

Key Takeaways

- Stablecoin payment integration lets a business send and accept fully-backed digital dollars — USDC, USDT, PYUSD — over public blockchains, settling in minutes instead of days.

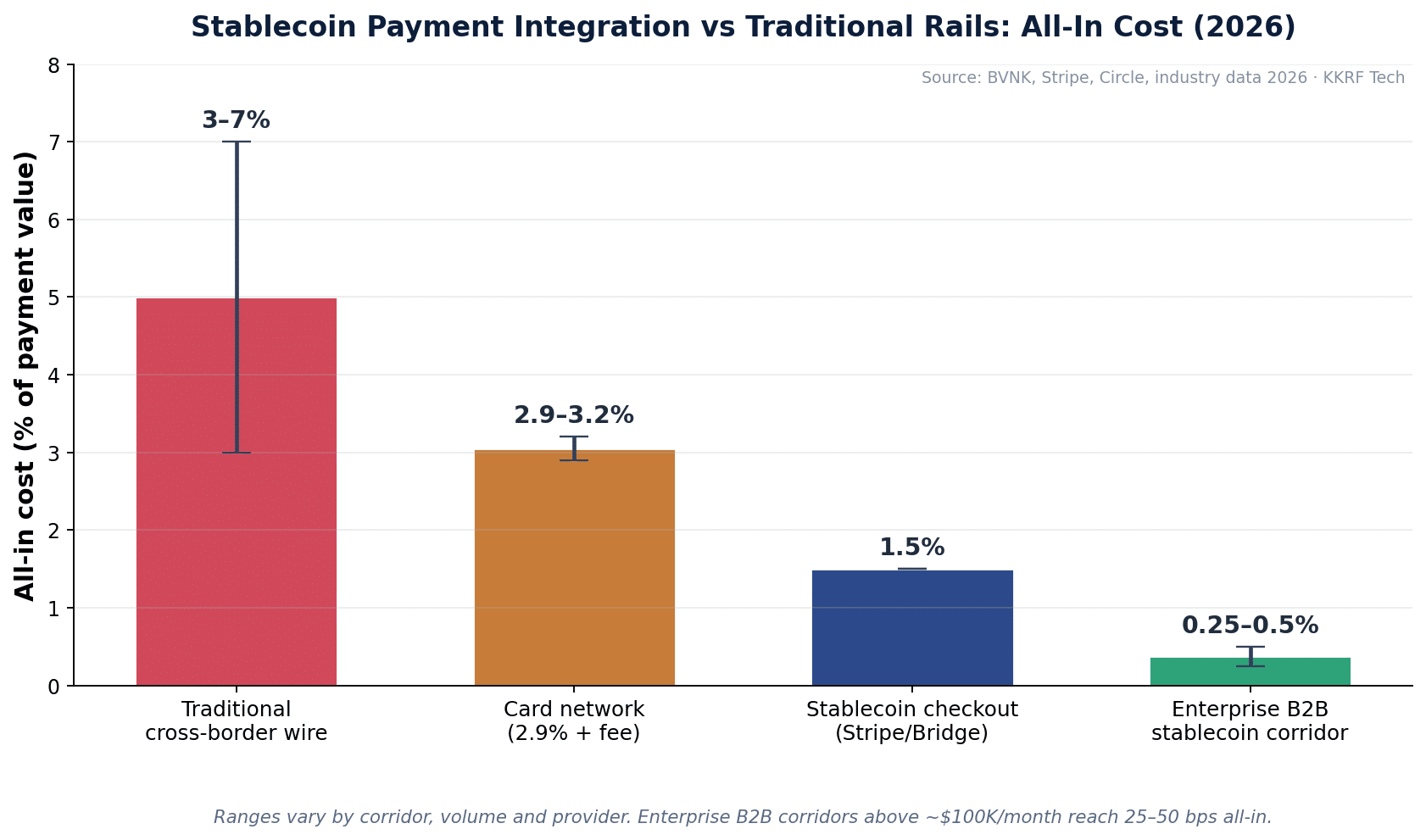

- Enterprise B2B corridors above roughly $100K per month now settle at 25–50 basis points all-in, versus 3–7% for traditional cross-border wires.

- The GENIUS Act (US, signed July 2025) and MiCA (EU, fully enforced in 2026) are the two governing frameworks — and their reserve rules are not mutually recognized.

- The hard engineering problems are not the payment itself but custody, idempotent reconciliation, OFAC and Travel Rule screening, and multi-chain routing.

- Stablecoins rarely replace card and wire rails outright; the 2026 best practice is a hybrid stack that routes each payment to the cheapest compliant rail.

In This Article

- What Is Stablecoin Payment Integration?

- Why Enterprises Are Adopting Stablecoin Payments Now

- How Stablecoin Payment Integration Works

- What Stablecoin Payment Integration Costs

- Comparing Stablecoin Payment Providers

- Security and Compliance Considerations

- The Enterprise Business Case and ROI

- Common Stablecoin Integration Mistakes

- Where Stablecoin Payments Are Heading

- When Stablecoin Payment Integration Makes Sense

- How to Evaluate a Development Partner

- Frequently Asked Questions

Quick Answer

Stablecoin payment integration is the process of connecting a company’s payment, treasury, or checkout systems to blockchain-settled digital dollars so value can move directly between parties. For most enterprises it is implemented through a regulated payment provider or orchestration API — such as Circle, Bridge, BVNK, or Fireblocks — that hides wallets, multi-chain routing, and compliance behind familiar REST endpoints and webhooks. Done well, it cuts cross-border settlement from days to minutes and all-in cost from several percent to well under 1%.

KKRF Tech is a leading blockchain development company that builds and integrates production payment systems for fintech and enterprise clients, spanning custody, compliance tooling, and multi-chain settlement. The guidance below reflects patterns we apply on real engagements, where the gap between a working pilot and a production rollout is usually reconciliation, key management, and regulatory screening — not the payment call itself.

What Is Stablecoin Payment Integration?

Stablecoin payment integration is the engineering and operational work of connecting business systems to blockchain-settled stablecoins so payments can be sent, received, screened, and reconciled automatically. It sits at the intersection of payments engineering, treasury operations, and financial compliance.

A stablecoin is a blockchain-based token designed to hold a constant value — almost always pegged 1:1 to a fiat currency such as the US dollar — by holding cash and short-term government securities in reserve. The most widely used are Circle’s USDC, Tether’s USDT, and PayPal’s PYUSD. Each is issued as a token standard (for example ERC-20 on Ethereum) that any compatible wallet, smart contract, or exchange can hold and transfer.

Integration is not a single API call. A production stablecoin payment integration typically stitches together six capabilities: an on-ramp that converts fiat to tokens, a wallet and custody layer that holds keys safely, an orchestration layer that selects a blockchain and routes the transfer, a compliance layer that screens counterparties and addresses, an off-ramp that settles back to local currency, and a reconciliation layer that writes clean records into the ERP or treasury system.

In short: stablecoin payment integration turns a public blockchain into a settlement rail that behaves, from the finance team’s perspective, like an unusually fast and cheap bank transfer.

Why Enterprises Are Adopting Stablecoin Payments Now

Adoption accelerated because the economics and the regulation finally arrived together. B2B stablecoin payment volume grew roughly 733% during 2025, and total stablecoin market capitalization crossed about $316 billion by March 2026 with more than 232 million holders worldwide. This is no longer a fringe rail.

Four forces are driving enterprise interest specifically. Speed: a cross-border transfer that takes two to five days over correspondent banking settles in minutes on-chain, 24/7, including weekends and holidays. Cost: traditional cross-border transfers carry 3–7% in FX markup, correspondent charges, and wire fees, while stablecoin corridors can drop the all-in cost below 1%.

Working capital: faster settlement frees cash that would otherwise sit in transit or in pre-funded nostro accounts. Regulatory clarity: the GENIUS Act in the United States and MiCA in the European Union have replaced ambiguity with defined rules for issuers, custodians, and the businesses that use them — which is exactly what enterprise risk committees were waiting for.

The takeaway: the case for stablecoin payment integration is strongest wherever money currently crosses a border, sits idle in transit, or pays a percentage-based intermediary.

How Stablecoin Payment Integration Works

At a reference-architecture level, a stablecoin payment moves through a predictable pipeline. Most enterprises never touch raw blockchain calls directly — a regulated provider or orchestration API exposes each stage as a REST endpoint with webhook callbacks, using the same patterns a team already applies to card processors.

- Funding and on-ramp. Fiat enters the system and is converted to a stablecoin, either by minting (e.g. Circle Mint) or purchasing through a liquidity provider.

- Wallet and custody. Tokens are held in wallets secured by MPC (multi-party computation) or HSM-backed key management, so no single person or server holds a complete private key.

- Compliance screening. Counterparties pass KYC/KYB, and every address is checked against OFAC sanctions lists and Travel Rule requirements before value moves.

- Chain selection and routing. The orchestration layer picks a blockchain — Ethereum, Base, Polygon, or Solana — balancing fees, settlement speed, and where the recipient can receive.

- Settlement and confirmation. The transfer is broadcast; a webhook fires on confirmation. Idempotency keys ensure a retried webhook never triggers a duplicate payment.

- Off-ramp or hold. The recipient either keeps the stablecoin as working balance or converts it to local currency through a regulated off-ramp.

- Reconciliation. Each transaction is written back to the ERP, accounting, or treasury system with amount, chain, hash, and cost basis for audit-ready records.

Custody is worth defining precisely, because it is where most security risk concentrates. Custody is the practice of storing and controlling the cryptographic keys that authorize movement of tokens. Enterprise-grade custody uses MPC or hardware security modules so that key material is split, never fully exposed, and governed by policy — spend limits, approvals, and allow-lists.

Section summary: the payment is the easy part. The architecture earns its keep in custody, idempotent confirmation, and clean reconciliation — the stages that keep money and books correct under real-world retries and failures.

What Stablecoin Payment Integration Costs

The all-in cost of a stablecoin payment is lower than card or wire rails, but it is not zero, and it is not a single number. Enterprise B2B corridors above roughly $100K per month typically land at 25–50 basis points all-in once enterprise pricing applies — against 3–7% for a traditional cross-border wire.

Real cost has four components. Provider fee ranges from 0 bps (Circle Mint) to around 250 bps on some retail off-ramps. Spread on multi-issuer flows can quietly add 10–40 bps. Network (gas) fees are usually cents on low-cost chains like Base, Polygon, or Solana. Off-ramp conversion to local currency runs 0.5–2% depending on the destination corridor.

Provider list pricing anchors the picture: Stripe’s Bridge-powered checkout charges about 1.5% on stablecoin acceptance (versus 2.9% + $0.30 for cards), BVNK and Conduit reach 25–50 bps for enterprise B2B corridors, and Circle Mint itself charges no provider fee. Build cost is separate: a focused production stablecoin payment integration is a multi-week engineering effort covering custody, compliance wiring, and ERP reconciliation — not a weekend plug-in.

Cost summary: budget for provider fee, spread, gas, and off-ramp — plus a real engineering integration. The savings are real but corridor-specific, so model your own volume rather than trusting a headline rate.

Not sure whether a stablecoin corridor actually beats your current wire and FX costs? We will model your real volume, corridors, and off-ramp fees so the business case is grounded in your numbers — not a marketing rate. Ask KKRF Tech for a cost model.

Get a Stablecoin Cost Model →Comparing Stablecoin Payment Providers

Most enterprises integrate through a provider rather than building on-chain plumbing from scratch. The right choice depends on your corridors, whether you need issuance or just acceptance, and how much compliance you want handled for you. The table below summarizes where the leading providers fit as of 2026.

| Provider | Best for | Coverage / chains | Indicative enterprise fee | Compliance notes |

|---|---|---|---|---|

| Circle (USDC / CPN) | Issuance, mint/redeem, orchestration | USDC across 20+ chains | 0 bps mint; network fees apply | US regulated issuer; GENIUS-aligned reserves |

| Bridge (Stripe) | Acceptance + LATAM off-ramp | USDC on Ethereum, Base, Polygon, Solana | ~1.5% checkout | Deep Mexico (SPEI) and Brazil (PIX) rails |

| BVNK | Enterprise B2B corridors, payroll, AP | Multi-chain, SEPA Instant | 25–50 bps all-in | EMI licenses UK/EU; Travel Rule built in |

| Fireblocks | Custody + treasury infrastructure | Broad chain and token support | Platform + policy-based pricing | MPC custody, policy engine, screening |

| Coinbase Commerce | Merchant acceptance, simpler setup | Major chains, USDC-first | ~1% acceptance | US-regulated; lighter enterprise tooling |

A practical rule: if you need to issue or hold large balances, start with Circle or Fireblocks; if you need to accept payments with minimal lift, Bridge or Coinbase Commerce; if your problem is high-volume cross-border B2B, BVNK and Conduit are built for exactly that.

Provider summary: match the provider to the job — issuance, acceptance, custody, or cross-border corridor — rather than defaulting to the best-known brand.

Security and Compliance Considerations

Compliance is now the decisive factor in enterprise stablecoin payment integration, because two major frameworks took force in this window. Ignoring either can strand a rollout.

The GENIUS Act (US, Public Law 119-27, signed 18 July 2025) classifies payment stablecoins as digital money and restricts issuance to permitted issuers. Reserves must be held in Federal Reserve credits, insured demand deposits, Treasury securities maturing in 93 days or less, or overnight repos backed by those bills. Implementation is phased: the OCC published a proposed rule in March 2026, FinCEN and OFAC issued a joint AML and sanctions proposal in April 2026, final rules are targeted for July 2026, and the full regime is expected to be operational from January 2027.

MiCA (EU) is in full enforcement, and stablecoin issuers must be authorized by 1 July 2026 or lose EU access. It requires segregated reserves, daily redemption rights, no interest on e-money tokens, and strict AML and KYC. Crucially, MiCA requires significant issuers to hold 60% of reserves as deposits at EU credit institutions — a requirement that conflicts with the GENIUS Act’s cash-and-T-bill model. No mutual recognition or equivalence agreement exists between the two regimes, so global operators must design for both.

On the security side, the recurring risks are key management, sanctioned-address exposure, and smart-contract flaws. Enterprise controls include MPC or HSM custody with policy-based approvals, continuous FATF Travel Rule and OFAC screening, allow-listing of counterparties, and independent audits of any custom on-chain code. Teams already investing in forward-looking cryptographic resilience — see our analysis of post-quantum cryptography migration — should fold key-management strategy into the same roadmap.

Compliance summary: treat GENIUS and MiCA as separate obligations, screen every address, and put custody under policy control. The regulation is now clear enough to build on — but not uniform across jurisdictions.

The Enterprise Business Case and ROI

The ROI of stablecoin payment integration is concentrated in cross-border flows. In current surveys, 41% of enterprise users report cost reductions of at least 10%, driven primarily by cross-border B2B payments. On a $50 million annual cross-border program, a 10% reduction is $5 million returned to the business every year.

Beyond direct fees, faster settlement improves working capital: cash that once sat in transit or in pre-funded accounts becomes available the same day. That matters most for supplier payments, contractor and payroll disbursement in emerging markets, treasury movement between entities, and marketplace payouts.

The honest counter-case: for purely domestic, card-based consumer checkout, stablecoins usually add complexity without saving much. ROI depends on corridor, volume, and how much manual reconciliation you eliminate — which is why a measured pilot beats a big-bang rollout.

Business-case summary: quantify savings on your real cross-border volume, add the working-capital benefit, and subtract integration and compliance cost. If the corridors are high-friction, the math usually clears easily.

Common Stablecoin Integration Mistakes to Avoid

These are the failure patterns we see most often when reviewing stablecoin integrations that stalled or had to be reworked.

- Treating it as a crypto project, not a payments project. The stakeholders that matter are treasury, compliance, and accounting — not just blockchain engineers.

- Skipping idempotency keys. Webhook retries without idempotency cause duplicate payments; this is the single most expensive bug in the category.

- Underestimating reconciliation. Cost basis, chain reorganizations, and partial confirmations all need handling before finance will trust the ledger.

- Ignoring off-ramp liquidity. A cheap transfer is worthless if the recipient cannot convert to local currency quickly at a fair rate.

- Weak key management. Single-server private keys or hot wallets without MPC/HSM custody are an audit and breach risk.

- Assuming one framework covers you. GENIUS-compliant reserves do not satisfy MiCA, and vice versa; plan for both if you operate across the US and EU.

- Hard-coding one chain or issuer. Without routing fallback, a single network congestion event or depeg scare can halt payments.

Where Stablecoin Payments Are Heading

The competitive landscape shifted sharply in mid-2026. On 30 June 2026, Stripe, Visa, Coinbase, BlackRock, and more than 140 other businesses announced backing for a new stablecoin network positioned to rival Tether and Circle — and Circle’s shares fell on the news. Expect issuer competition, not a single winner, to define the next phase.

Three technical trends follow from that. Bank-issued and consortium stablecoins will proliferate under GENIUS-style rules, pushing integration toward issuer-agnostic routing. ERP-native integration will deepen, with stablecoin settlement appearing directly inside treasury and AP workflows. And programmable payments — conditional release, automated AR/AP, and machine-to-machine or agentic payments — will move from demos to production.

The balancing risk: more issuers and networks mean more fragmentation, more depeg and counterparty questions, and more compliance surface. Architectures that abstract the issuer and chain behind a routing layer will age far better than those wired to a single token.

Forward view: bet on abstraction. The winning integrations treat any single stablecoin or chain as replaceable, and keep compliance and routing as first-class, swappable layers.

When Stablecoin Payment Integration Makes Sense

Stablecoin payment integration is a strong fit for some payment problems and a poor fit for others. Use the framework below before committing budget.

Strong fit

- High-volume cross-border B2B payments where wire fees and FX markup are eating margin.

- Supplier, contractor, or payroll disbursement into emerging markets with slow or costly banking.

- Treasury movement between entities or geographies that needs to settle same-day.

- Marketplaces and platforms making frequent, low-margin payouts.

Weak fit

- Purely domestic, card-based consumer checkout with no cross-border component.

- Low cross-border volume where integration and compliance cost outweighs savings.

- Organizations without the compliance capacity to run KYC/KYB, OFAC, and Travel Rule screening.

As an experienced blockchain and custom software development company, KKRF Tech generally recommends enterprises begin their stablecoin payment integration with a single high-friction corridor, run it alongside the existing rail for about 30 days, and compare cost, speed, and reconciliation effort before scaling — then keep traditional rails wherever they are already efficient in a deliberate hybrid stack.

Decision summary: pilot one corridor, measure honestly, and adopt a hybrid stack. Let the data — not enthusiasm — decide how far the rollout goes.

How to Evaluate a Stablecoin Development Partner

Whether you build in-house or engage a firm, judge stablecoin payment integration capability against a concrete checklist rather than crypto buzzwords.

- Regulated-provider experience integrating Circle, Bridge, BVNK, Fireblocks, or equivalents — not just raw on-chain code.

- Custody and key management using MPC or HSM with policy-based approvals.

- Compliance engineering: demonstrable OFAC screening, Travel Rule, and KYC/KYB wiring.

- ERP and treasury integration with audit-ready reconciliation, not just a payment demo.

- Multi-chain routing and issuer-agnostic design for resilience.

- Security auditing of any custom smart contracts or middleware.

- Production references — real deployments handling real value, with lessons to share.

Planning a compliance-ready stablecoin rollout across US and EU corridors? KKRF Tech designs custody, screening, and reconciliation so your integration passes audit on day one. Explore our blockchain development services or bring us your target corridors.

Talk to Our Blockchain Payments Team →Frequently Asked Questions

Are stablecoin payments legal for businesses in 2026?

Yes. In the US, the GENIUS Act (signed July 2025) provides a federal framework for payment stablecoins, with implementing rules being finalized through 2026 and the full regime expected operational from January 2027. In the EU, MiCA is in force and requires issuers to be authorized by 1 July 2026. Businesses can use compliant stablecoins today, provided they use regulated providers and run proper KYC, AML, and sanctions screening.

How much does stablecoin payment integration cost?

Transaction cost for enterprise B2B corridors typically runs 25–50 basis points all-in, versus 3–7% for traditional cross-border wires. On top of transaction cost, budget for a multi-week engineering integration covering custody, compliance, and ERP reconciliation. Exact savings depend on your corridor, volume, and off-ramp currency.

Which stablecoin should an enterprise use — USDC or USDT?

For most US and EU enterprises, USDC is the common default because Circle is a regulated issuer with reserve transparency and broad institutional support. USDT has deeper liquidity in some emerging-market corridors. The stronger architecture stays issuer-agnostic, routing through whichever compliant stablecoin best fits the corridor rather than hard-coding one.

Do you need to hold cryptocurrency to accept stablecoin payments?

No. Providers like Bridge, BVNK, and Coinbase Commerce can auto-convert incoming stablecoins to local currency at settlement, so the business never holds a crypto balance. Companies that want the working-capital and speed benefits can choose to hold stablecoins, but it is optional.

How are refunds and chargebacks handled with stablecoin payments?

Blockchain transfers are final and have no card-style chargeback mechanism. Refunds are handled as new outbound payments, and disputes are managed at the application and contract layer rather than by the network. This removes fraudulent-chargeback risk but shifts responsibility for dispute policy onto the merchant, which should be designed in from the start.

How long does a stablecoin payment integration take to build?

A focused production integration for one or two corridors is typically a multi-week effort. The payment API itself is quick; the time goes into custody setup, compliance screening, off-ramp configuration, and reconciliation into existing finance systems. Starting with a single corridor pilot shortens time-to-value considerably.

Ready to move from research to a working pilot? KKRF Tech builds and operates enterprise-grade stablecoin payment integration end to end — custody, compliance, routing, and reconciliation. Start with one corridor and prove the numbers.

Book a Stablecoin Integration Consultation →